News Arts & Entertainment 'The White Lotus': Tell us your finale theories April 2, 2025 Automotive Montclare Automotive Corp: Delivering Trusted Auto Repair Services to Chicago Drivers January 23, 2025 Books & Literature Can’t Wait Wednesday 4/2/25 April 2, 2025 Building & Construction 12 Best Bar Cabinet Picks For the Perfect In-Home Coffee Bar 2025 April 2, 2025 Business Trump claims his tariffs are ‘kind’ to other countries. In America, consumers will ‘feel the pinch quite quickly,’ top economist says April 2, 2025 Cryptocurrency Former New York governor advised OKX over $505M federal probe: Report April 2, 2025 Education 26 Free Interactive Budgeting Activities for High School Students April 2, 2025 Family & Parenting This mom’s monologues to her baby aren’t just going viral—they might actually rewire baby’s brain April 2, 2025 Fashion & Beauty Trump’s Tariffs Rock Fashion’s Supply Chain April 2, 2025 Finance USD / CAD – Canadian dollar awaiting tariff shoe to drop April 2, 2025 Foreign Language Bijouterie Hidous : Luxe intemporel et bijoux personnalisés au cœur de Montréal March 2, 2025 Gov & Politics No post found! Health & Fitness Supreme Court rules for the FDA in flavored vapes dispute April 2, 2025 Home & Garden Transform Your Bathroom with Wake Forest Bath’s Expert Renovation Services July 16, 2024 Lifestyle Petals in Paradise: An orchid wonderland awaits April 2, 2025 Real Estate Steve Cohen sweetens casino proposal with 450 affordable units April 2, 2025 Religion Marshall Faulk Presents New Orleans Youth With Epic Mural February 18, 2025 Science SpaceX's Fram2 launch sends civilian crew into flight around Earth's poles March 31, 2025 Sports LAFC vs. Inter Miami pick, where to watch, live stream: Prediction, odds, will Lionel Messi play? April 2, 2025 Technology Space solar startup Aetherflux raises $50M to launch first space demo in 2026 April 2, 2025 Travel Little girl discovers 3,800-year-old amulet with ties to Biblical people during family trip April 2, 2025

Montclare Automotive Corp: Delivering Trusted Auto Repair Services to Chicago Drivers January 23, 2025

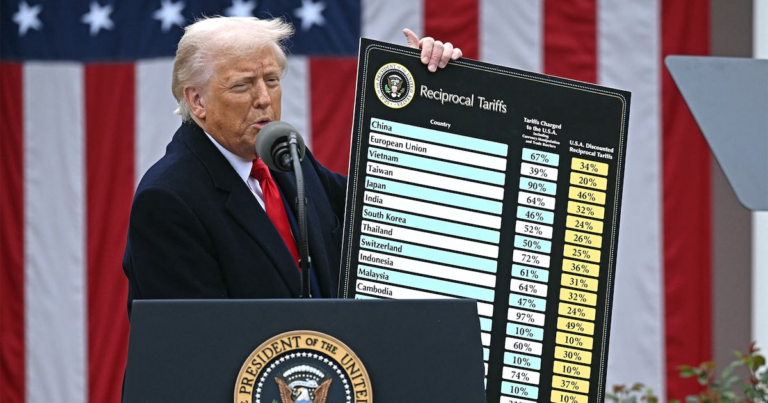

Trump claims his tariffs are ‘kind’ to other countries. In America, consumers will ‘feel the pinch quite quickly,’ top economist says April 2, 2025

This mom’s monologues to her baby aren’t just going viral—they might actually rewire baby’s brain April 2, 2025

LAFC vs. Inter Miami pick, where to watch, live stream: Prediction, odds, will Lionel Messi play? April 2, 2025

Little girl discovers 3,800-year-old amulet with ties to Biblical people during family trip April 2, 2025